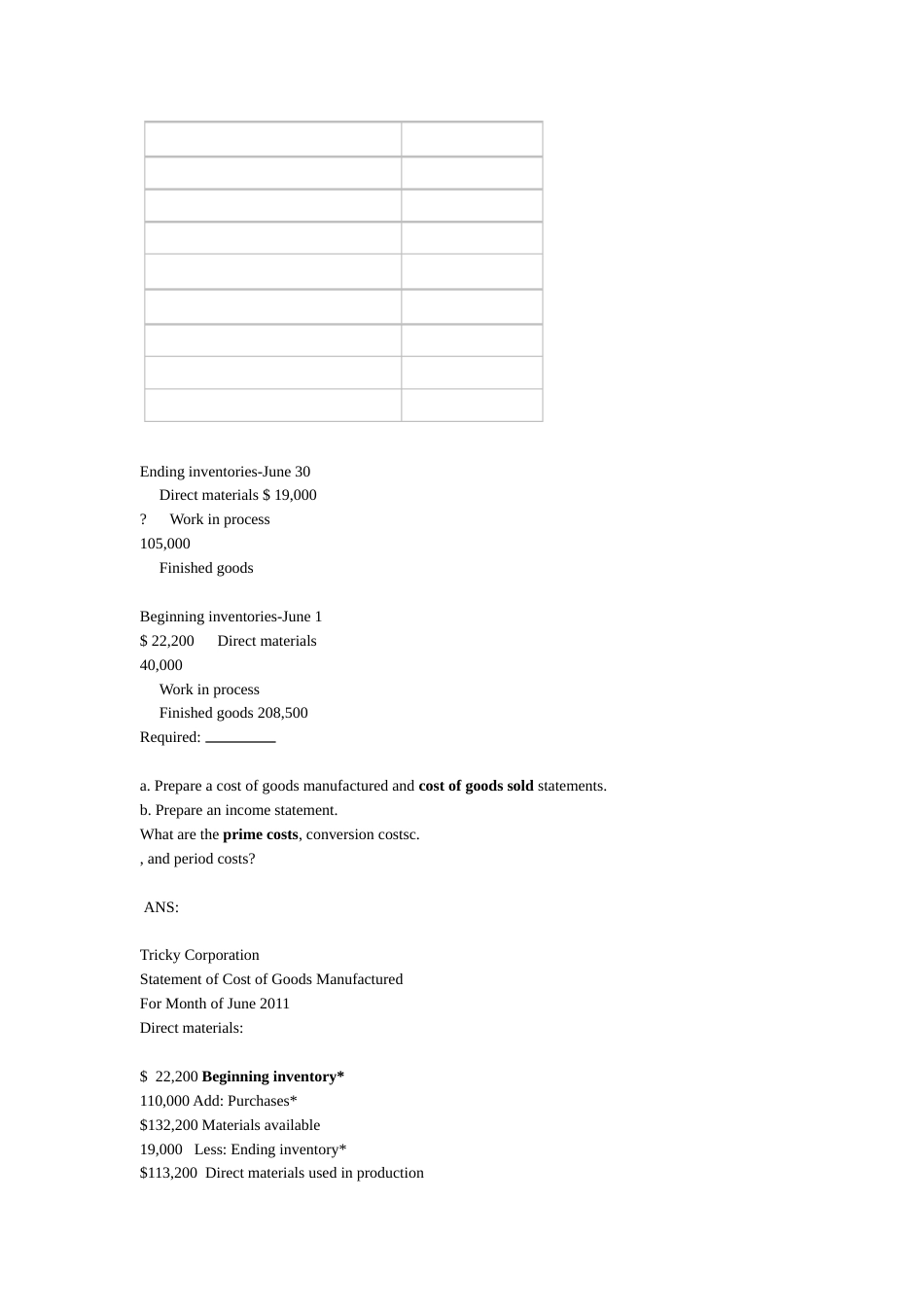

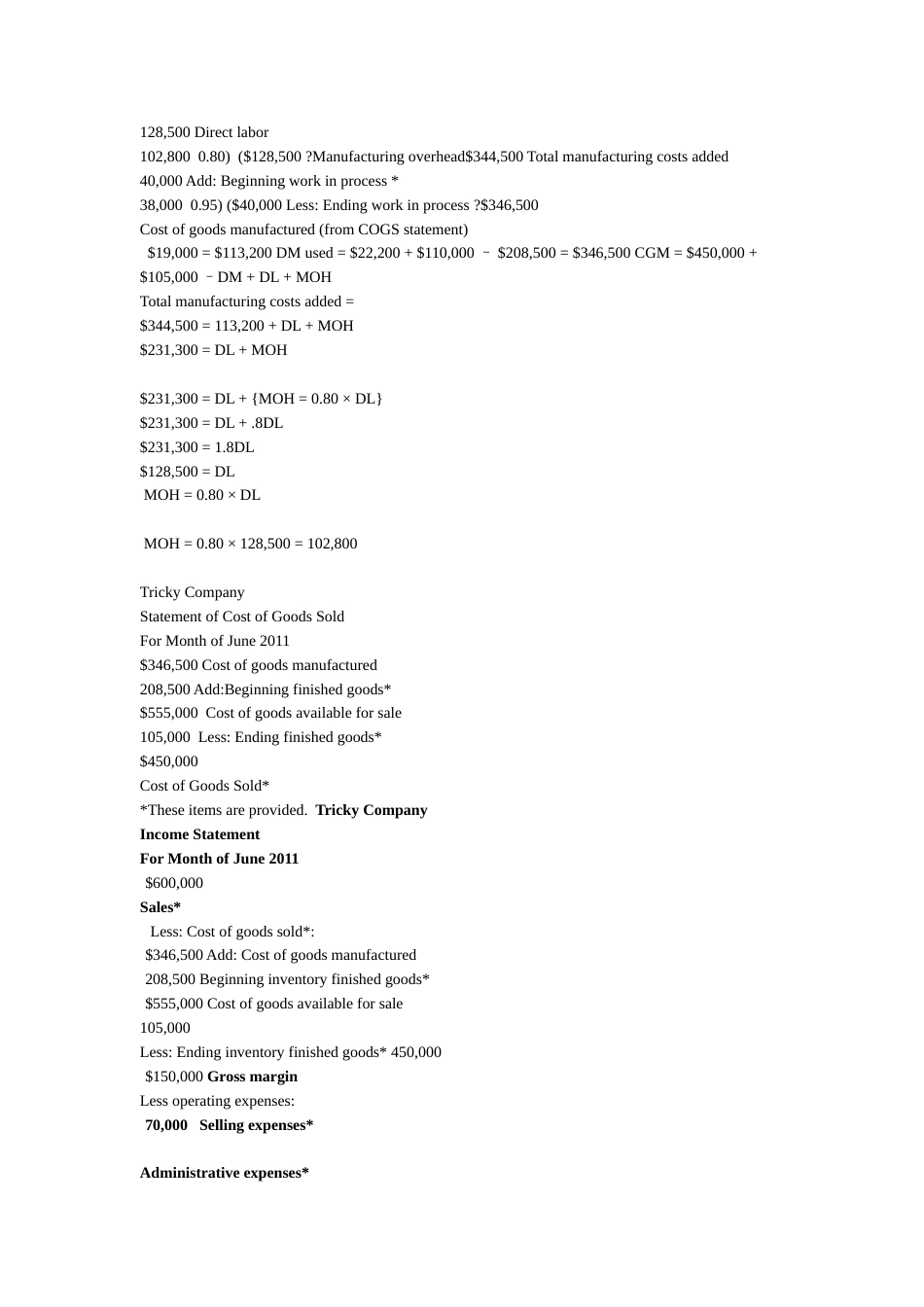

CHAPTER1INTRODUCTIONTOCOSTACCOUNTINGidentifies,collects,measures,classifies,andreportsinformationthatisusefultocostmanagement:managersincosting(determiningwhatsomethingcosts),planning,controlling,anddecisionmaking成本会计是收集、整理成本信息,计算产品、劳动等成本对象的成本,并什么是成本会计:利用成本信息来编制企业的财务报表、进行成本控制和为企业的内部经营与决策踢空依据的管理活动。问答:ExplaintherelationshipbetweentheFinancialAccountingSystemandtheCostManagementSystem?Afinancialaccountingsystemismainlyconcernedwithproducinginformationforthe答案:company'sexternalusers.Financialaccountinginformationisusedforinvestmentdecisions,stewardshipevaluation,activitymonitoring,andregulatorymeasures.TherulesthatgovernafinancialaccountingsystemaredefinedbytheSecuritiesExchangecommission(SEC)andtheFinancialAccountingStandardsBoard(FASB).Outputsofafinancialaccountingsystemincludethestandardfinancialstatementswhichincludetheincomestatement,balancesheet,andthestatementofcashflows.nagementsystemisconcernedwithproducinginformationforthecompany'sThecostmainternalusersandisdesignedtomeetmanagementobjectives.Acostmanagementsystemhasthreebroadobjectives-toprovideinformationon:costingofproductsandservices,planningandcontrolactivities,anddecisionmakingactivities.CHAPTER2BASICCOSTMANAGEMENTCONCEPTS基本概念:mayTheycostsanythingforwhicharemeasuredandassigned.areCostObjects?include:products,customers,departments,projects,activities,andsoon.abicycleisacostobjectwhenyouaredeterminingthecosttoproduceaExample:bicycle.Abasicunitofworkperformedwithinanorganization.Activity:?settingupequipment,movingmaterials,maintainingequipment,andExample:designingproducts.Coststhatcannotbeeasilyandaccuratelytracedtoacostobject.Indirectcosts:?thesalaryofaplantmanager,wheredepartmentswithintheplantare:Exampledefinedasthecostobjects.Coststhatcanbeeasilyandaccuratelytracedtoacostobject.Directcosts:?thesalaryofasupervisorofadepartment,wherethedepartmentisdefined:Exampleasthecostobject,orbricksdeliveredtoahousethatisbeingconstructedbyacontractor,wherethehouseisthecostobject.Traceability:Theabilitytoassignacosttoacostobjectinaneconomicallyfeasible?waybymeansofacausalrelationship.Thefactorsthatcausechangesinresourceusage,activityusage,cost,andDriver:?revenues.Theleastaccuratecostassignmentmethod.Often,nocausalrelationshipAllocation:?existsbetweenthecostandthebasisusedtoassignthecosttothecostobject.Assignmentofindirectcoststocostobjectsiscalledallocation.PrimeCostisthesumofdirectmaterialscostanddirectlaborcost.ConversionCostisthesumofdirectlaborcostandoverheadcost.EXTERNALFINANCIALSTATEMENTSIncomestatementrelyon:CostofgoodsmanufacturedCostofgoodssoldProductioncostsareassignedtoproductsorservicesanddonotbecomeexpensesuntilthepointofsale.Marketingandadministrativecostsareperiodcostsandaredeductedasanexpenseontheincomestatementintheperiodincurred.Nonproductioncostsdonotappearonthebalancesheet.Example:ThecostofgoodssoldfortheTrickyCorporationforthemonthofJune2011was$450,000.Work-in-processinventoryattheendofJunewas95percentofthework-in-processinventoryatthebeginningofthemonth.Overheadis80percentofthedirectlaborcost.Duringthemonth,$110,000ofdirectmaterialswerepurchased.RevenuesforTrickywere$600,000,andthesellingandadministrativecostswere$70,000.OtherinformationaboutTricky'sinventoriesandproductionforJunewasasfollows:Endinginv...